Witnesses provided the Committee with their

views about the primary mechanism by which many Canadians voluntarily save for

their retirement in a tax-assisted manner—RRSPs—as well as about new mechanisms that might be implemented to

enhance voluntary retirement saving. With voluntary measures, Canadians often

make their own investment decisions, and better decisions are typically made

when the level of financial literacy is high; witnesses also provided their

views on literacy.

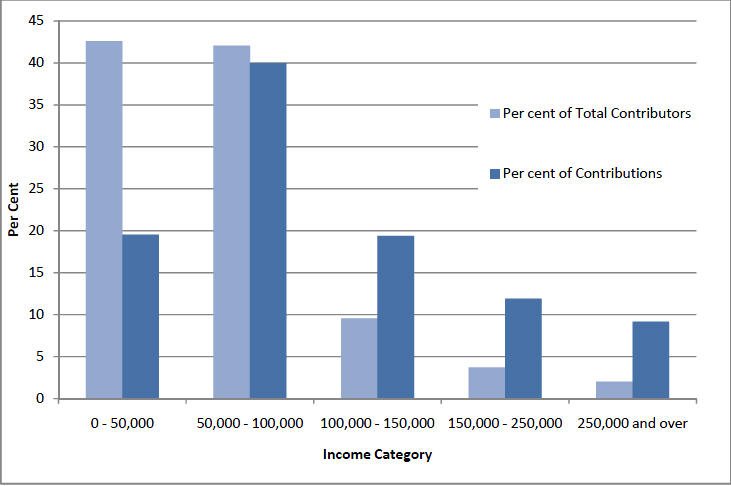

Figure 3: Total Contributions and Total Contributors to

Registered Retirement

Savings Plans, by Income Category, 2008 Taxation Year (%)

Source: Canada Revenue Agency, Income Statistics 2010—2008 tax year,

http://www.cra-arc.gc.ca/gncy/stts/gb08/pst/ntrm/pdf/table2-eng.pdf.

The BMO Financial Group’s Ms. Tina Di Vito

told the Committee that, in 2005, Canadians saved 1.2% of personal income, a

figure that had risen to 4.8% in 2008. She also indicated, however, that

Canadians are living longer, healthier lives, thereby giving rise to a need for

more saving to sustain them in what was characterized by her as a long and

active retirement. Ms. Di Vito also commented that: about 38% of Canadians

participate in an occupational pension plan, some of which are defined

contribution plans that involve a relatively greater burden for individuals in

terms of adequacy of saving and management of the investments; the costs of

care-giving are rising rapidly, giving rise to additional saving requirements to

meet their own needs as well as those of their parents; households headed by

baby boomers have more household debt than previous generations, with a

record-high level of household debt-to-income of about 145%; and the lifestyle

expectations of retirees are likely to exceed those of previous generations,

giving rise to a need for more retirement saving.

Ms. Di Vito also supported an increase in the

maximum contribution limit to RRSPs, questioning whether the current annual

limit is reasonable under the circumstances. She noted that, if RRSP

investments perform less well than expected, there is no ability to make

additional contributions to ensure that retirement is funded to the desired

level. In her opinion, the current limit also favours households, with a

dual-earner couple earning $75,000 each, for $150,000 in total, being able to

contribute $27,000 to their RRSPs and a single person earning $150,000 being

permitted to contribute $22,000. She argued for a contribution limit similar to

that of defined benefit pension plans.

Carleton University’s Mr. Ian Lee, who

appeared on his own behalf, identified annual limits on retirement saving as an

issue, and advocated a “levelling of the pension playing field” through the

creation of a common set of pension rules and replacement of the annual

contribution limit with an accumulated target, such as $1 million. Similarly

wishing to support equity, Mr. Scott Perkin, of the Association of Canadian

Pension Management, and Mr. Leslie Herr, of the Empire Life Insurance Company, urged

the adoption of a lifetime contribution limit in order to ensure greater parity

between those who save exclusively through an RRSP and those who are

occupational pension plan members. Mr. Terry Campbell, of the Canadian Bankers

Association, noted that while it is possible to carry forward unused RRSP contribution

room, it is tied to employment income; when you are younger, the contribution

room is lower. In Ms. Di Vito’s opinion, the ability to carry forward unused

contribution room is akin to a lifetime maximum contribution limit.

The annual RRSP contribution limit is based

on earned income, and Mr. Dean Connor, of the Canadian Life and

Health Insurance Association, advocated an expanded definition of “earned

income” to include such income sources as royalties and active business income.

In his view, such an expansion would benefit self-employed persons.

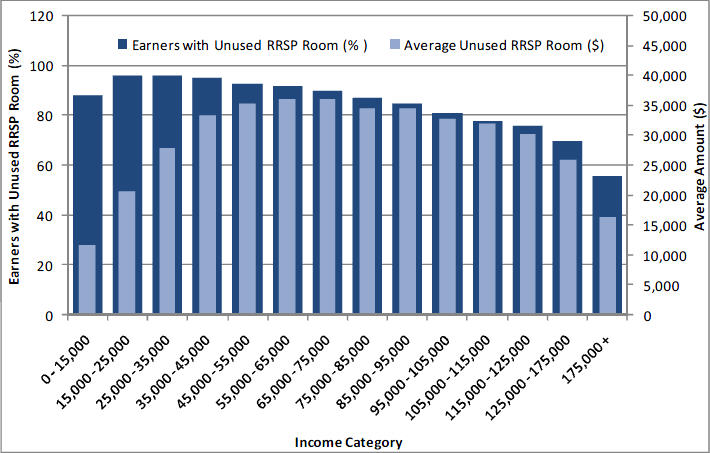

Figure 4: Earners with Unused Registered Retirement Savings

Plan Contribution

Room (%) and Average Amount of Unused Registered Retirement Savings Plan

Contribution Room, by Income Category, 2006

Source: Submission by the Department of Finance to the Standing

Senate Committee on Banking, Trade and Commerce, March 31, 2010.

Mr. Lee identified the trade-off that occurs

between retirement saving and other purchases, with specific mention made of

home ownership. In his view, the single largest asset for many Canadians is

their home, rather than their retirement saving. In Ms. Di Vito’s

opinion, however, Canadians are relatively reluctant to move out of their home

in old age; moreover, the amount of equity associated with the downsizing of a

home is often less than anticipated.

Some witnesses who commented on RRSPs also

spoke about registered retirement income funds (RRIFs), since contributions to

RRSPs must cease at age 71, and contributions and accumulated returns must be

used to purchase annuities or converted to RRIFs. For example, in recognizing

that Canadians live, work and save longer, and in implicitly supporting an end

to the practice whereby contributions to RRSPs must cease at age 71, Ms. Di

Vito also advocated flexibility for Canadians that would allow them to choose

when to begin withdrawing funds from their RRSPs.

In Ms. Di Vito’s view, flexibility should

also be given in respect of the mandatory minimum withdrawal rates from RRIFs.

In particular, she argued that the current prescribed withdrawal rates may

deplete RRIF funds too quickly, and advocated a reduction in the rate at which

funds must be withdrawn, which will extend the life of an RRIF. She commented

that withdrawal rates of 4% or 5% may be more sustainable.

Mr. Campbell, Mr. Herr and Mr. Connor

supported an increase in the age of conversion, with specific mention made of

an increase from 71 years to 73 years in order to allow those who are still

working to continue to save.

Witnesses also provided their views about a

range of other RRSP-related issues. For example, Ms. Di Vito suggested that

while RRSP contributions should be taxed as deferred employment income, the

investment returns generated by RRSP contributions should be taxed at a rate

that mimics the tax rate that would have been paid had the investments been

held outside a registered savings plan. For example, the investment returns

would be taxed as dividends and as capital gains, with preferential tax

treatment, rather than as interest income. In her view, the loss of preferred

tax status for dividend income and capital gains held in an RRSP affects

investment behaviour and may induce people to hold interest-bearing securities,

even if interest rates are relatively low.

Ms. Di Vito also commented that any balances

in RRSPs or RRIFs when individuals die should be permitted to be rolled over,

on a tax-free basis, into the next generation’s RRSP or RRIF. In her view,

ideally this rollover would be available in addition to any unused RRSP

contribution room. She also argued for a review of the 1995 Income Tax Act amendment that ended the ability to roll over a certain amount of severance

payments to an RRSP on a tax-free basis.

Neither Mr. Connor, nor Mr. John Farrell of

Federally Regulated Employers—Transportation and Communications (FETCO),

supported increases to OAS or GIS benefits; nor did they support increases to

the Canada/Quebec Pension Plan (C/QPP). Rather, they each endorsed some form of

a voluntary defined contribution supplement to the CPP. However, FETCO’s Mr. Ian Markham

warned that a voluntary CPP supplement, which would be on a defined

contribution basis, would redirect money that would otherwise have been contributed

to an RRSP. However, since RRSP investments are often made in relatively high-cost

investment vehicles, a voluntary supplement to the CPP could theoretically be

administered at a lower cost.

The Rotman International Centre for Pension

Management’s Mr. Keith Ambachtsheer, who appeared on his own behalf,

shared his view that Canadians do not, and probably will not, voluntarily

accumulate sufficient retirement saving; consequently, policy intervention is

needed. However, he had concerns about increasing mandatory contributions, and

referred to his proposal—discussed in the 2008 C.D. House Institute report The

Canada Supplementary Pension Plan—for a voluntary defined contribution

Canada Supplementary Pension Plan (CSPP); according to this proposal,

individuals would be automatically enrolled with pre-set contribution rates and

a target pension equivalent to a 60% post-employment earnings replacement rate.

The proposal included the ability to opt out, a number of annuitization

choices, and the ability to transfer RRSP assets into their CSPP personal

retirement savings account.

Mr. Connor was among the witnesses who spoke

to the Committee about the need for financial literacy. For example, he said

that education could improve the retirement savings habits of Canadians, and

advocated opportunities to enhance communication about the importance of

retirement saving, especially for younger Canadians who can establish lifetime

strategies that will ideally result in a financially secure future. Mr. Campbell

identified a need for enhanced financial literacy in respect of savings and

retirement planning, while Mr. Markham commented that many Canadians do not

understand how to invest their RRSPs, with the result that they tend to invest

in fairly high-cost vehicles and may make the wrong decisions. Mr. Herr noted

that Canadian consumers need to have easy access to accurate, timely and

understandable information designed to help them with their financial planning

needs. Finally, Mr. Ambachtsheer, argued that the average Canadian is not

well-versed in investment theory.