FINA Committee Report

If you have any questions or comments regarding the accessibility of this publication, please contact us at accessible@parl.gc.ca.

CHAPTER SIX: IMPROVING CANADA’S TAXATION AND REGULATORY REGIMESA. Background1. Personal Income TaxationProgressive marginal income tax rates for income earned by an individual have been part of the Canadian tax system since personal income taxes were created in the Income War Tax Act, 1917. Personal income taxes make the largest contribution to federal tax revenue, and comprised approximately 62% of total federal tax revenue in 2013–2014. For the 2014 taxation year, federal personal income tax rates range from 15% to 29%. These rates are applied on taxable income, which is total income minus deductions, with non‑refundable tax credits subtracted from the tax that is payable. Refundable tax credits, which are available even in the absence of taxable income and are calculated separately from non-refundable credits, are based on family income. In Canada, taxation is based on an individual, rather than on a family. That said, tax incentives may be shared between spouses or common-law partners, such as with personal tax credits, and family income may be considered in determining eligibility for certain government programs, such as the Canada Child Tax Benefit. 2. Corporate Income TaxationIn Canada, corporations have had their annual net income taxed since 1916; corporate income taxes are the second most significant contributor to federal tax revenue, and represented approximately 17% of total federal tax revenue in 2013–2014. Canadian-resident corporations are obliged to pay tax on their taxable income earned worldwide, while foreign corporations pay tax on their taxable income earned in Canada. Provided that there is a reasonable expectation of profit, companies may deduct – from their accrued revenue – the expenses incurred in producing goods and services. Current expenditures are deductible in the year in which they are incurred, while the cost of purchasing capital goods can be deducted from revenue over time in accordance with prescribed rates of deduction, or capital cost allowance rates. As well, interest on borrowings for the purpose of earning income from a business is deductible, as are business losses. Table 1 shows federal corporate income tax rates for the 2000 to 2014 taxation years. The corporate tax rate on general income is applied on corporations that are not eligible for size- and/or sector-specific corporate income tax rate reductions; it includes the general rate reduction for that taxation year, with this rate available to all Canadian-resident corporations. Two of the most common reductions are the manufacturing and processing credit and the small business deduction. Table 1 – Federal Corporate Income Tax Rates, Canada, 2000–2014 (%)

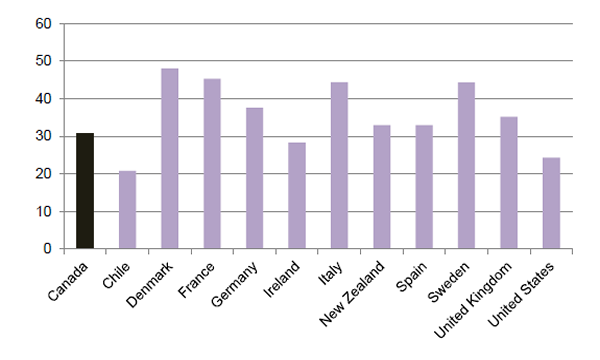

Source: Table prepared using information from: Income Tax Act, R.S.C. 1985, c. 1 (5th Supplement), various years. 3. Consumption and Excise TaxesSince 1991, the federal government has imposed the Goods and Services Tax (GST) on almost every sale of goods and services in, and import of such goods and services into, Canada. The GST, which is a value-added tax that is currently applied at the rate of 5%, is a tax on final consumption; businesses may be able to claim an input tax credit for purchases that are related to their business activities. That said, the tax is not imposed on GST-exempt goods and services, and it is applied at a rate of 0% on certain goods and services, such as basic groceries and exports; in relation to the latter, the term “zero-rated” is sometimes used. Retailers of the former are not allowed to claim an input tax credit for purchases that are related to the production of those goods and services, while retailers of the latter are allowed to claim the credit. As well, the federal government obtains revenue from the excise taxes or duties applied on the sale and import of specific goods, including alcohol, tobacco, gasoline and diesel fuel, and certain other goods and services. Customs duties may also be applied on goods imported into Canada. 4. Tax CompetitivenessSome commentators use tax competitiveness – the tax burden imposed on businesses and individuals resident in one country relative to that burden in one or more other countries – to assess the extent to which businesses and people might find a particular country desirable as a destination for foreign investment or residency respectively. Figure 12 shows, for 2012, total tax revenue at the national and subnational level as a percentage of gross domestic product in selected countries. Figure 12 – Total Tax Revenue as a Percentage of Gross Domestic Product, Selected Countries, 2012 (%)

Notes: “Total tax revenue” includes subnational taxes, social security contributions and payroll taxes.

Source: Figure prepared using information from: Organisation for Economic Co-operation and Development, Tax Statistics. 5. Tax ComplianceLike a number of other countries, Canada wants a tax system that is fair for taxpayers and that protects the revenue base. To ensure that the tax system meets these goals, taxpayers must comply with tax laws, which give rise to a compliance burden. The Canada Revenue Agency has estimated that, for 2010–2011, 17.6% of “key tax credits or deductions” claimed by individuals were disallowed following a review of eligibility for, or the amount of, the credit or deduction. Regarding audits of small- and medium-sized companies, for 2007–2008, the Agency adjusted the tax returns of 27.5% of these companies; the adjustments averaged $6,000. In general, countries use a territorial system of taxation for foreign branches of domestic companies; this system defers the domestic taxation of income earned by a foreign branch until that income is repatriated as dividends paid to an individual taxpayer. Governments are concerned about the international taxation of multinational companies, as these companies may attempt to access favourable tax laws in certain jurisdictions in an effort to reduce their overall tax liability. In September 2014, the Organisation for Economic Co-operation and Development (OECD) and the Group of Twenty nations released recommendations that address base erosion and profit shifting by multinational companies. 6. The Costs of Regulation to BusinessesRegulations, which are a main instrument used by governments to achieve policy objectives, contain principles, rules or conditions that govern the behaviour of residents and businesses. According to the Standard Cost Model that is used by the OECD, businesses incur two types of costs as a result of regulations: financial and compliance. In Canada, the Cabinet Directive on Regulatory Management provides the primary policy framework for making federal regulations. According to the Directive, when new regulations are implemented, departments and agencies must maintain the net number of regulations and the net administrative burden on businesses, a practice that is known as the “one-for-one” rule. Additionally, when regulations are being designed, departments and agencies must consider the impact of the proposed regulations on small businesses. Figure 13 shows the average annual cost of regulatory compliance for Canadian businesses of various sizes in 2005, 2008 and 2011. Figure 13 – Average Annual Cost of Regulatory Compliance for Businesses, Canada, by Number of Employees in the Business, 2005, 2008 and 2011 (constant dollars 2011)

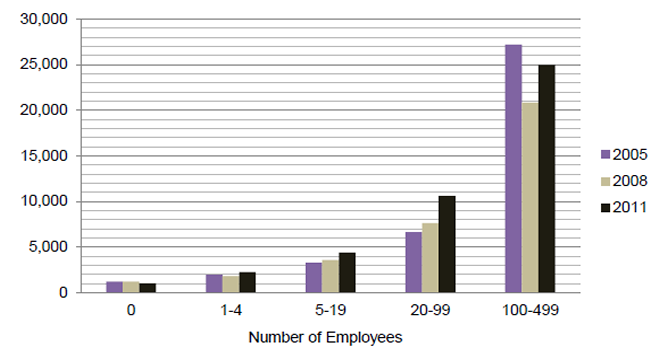

Note: The regulatory compliance cost includes the administrative costs associated with: payroll remittances for Employment Insurance and Canada Pension Plan contributions; Government of Canada Record of Employment; T4 and RL forms for employee income taxes; workers’ compensation remittances and claims; federal/provincial income tax and sales tax filings; corporate registration; Statistics Canada surveys; municipal and provincial licences and permits; and other regulations. Source: Figure prepared using information from: Government of Canada, SME Regulatory Compliance Cost Report, September 2013. B. Changes Proposed by Witnesses Invited to Address “Improving Canada’s Taxation and Regulatory Regimes”Witnesses invited by the Committee to speak about the topic of improving Canada’s taxation and regulatory regimes commented on a range of issues. In relation to the tax system, they focused on tax revenue, tax simplification, reform and compliance, international taxation, and the tax treatment of certain businesses, entities and individuals. Regarding Canada’s regulatory regime, they mentioned credit card transaction fees, securities, charities, and financial services provided by the federal government. 1. Tax Systema. Tax RevenueIn highlighting methods to increase federal tax revenue, the Canadian Centre for Policy Alternatives requested a broadening of the tax base by: extending the Goods and Services Tax to financial activities and services; capping lifetime contributions to tax shelters, such as Tax-Free Savings Accounts; introducing an inheritance tax; eliminating the deduction for stock options and for capital gains; increasing tax compliance; and improving the identification and prosecution of tax crimes. Similarly, Canadians for Tax Fairness supported measures to increase federal tax revenue, and proposed that tax loopholes that disproportionately benefit high-net-worth individuals and raise income inequality be closed; particular mention was made of the deduction for employee stock options. It also called for an evaluation of previous tax incentives to determine their effectiveness, with this evaluation occurring prior to the introduction of new measures. b. Tax Simplification, Reform and ComplianceIn commenting on the increase in the number of tax provisions since 1987, and on the United Kingdom’s permanent and independent tax simplification office, Arthur Cockfield – who is with Queen’s University and appeared as an individual – advocated the creation of an independent expert panel to provide advice on short- and long-term options to streamline Canada’s tax system. The Chartered Professional Accountants of Canada made a similar proposal. Mr. Cockfield also spoke about the level of taxation, suggesting that the tax base be broadened, and the number of tax shelters and loopholes be reduced; the tax rate could perhaps be reduced at the same time. Mike Moffat – who is with Western University and appeared as an individual – proposed a reduction in tax rates, especially for the lowest tax bracket, instead of multiple tax incentives for low-income individuals. The Chartered Professional Accountants of Canada mentioned what is commonly known as the Carter Commission, which comprehensively examined the Income Tax Act in the 1960s, and suggested that – due to the increased mobility of capital – the entire tax system be examined to determine whether the existing balance among consumption, corporate income and personal income taxes is appropriate. In speaking about tariffs and the high administrative burden imposed on businesses – especially small- and medium-sized businesses – to obtain the most-favoured-nation rate, Mr. Moffat proposed that this rate be reduced to zero for tariff items with a very low effective tariff rate. Regarding the administrative burden imposed on non-residents that provide services to Canadian corporations, Tax Executives Institute, Inc. highlighted that the Income Tax Act requires the non-resident to pay the withholding tax unless a form is filed with the Canada Revenue Agency. It asked for a self-certification system for non-residents in cases where there is an applicable tax treaty that reduces the withholding tax to zero. Moreover, Tax Executives Institute, Inc. identified electronic filing as an important means by which to reduce compliance costs for businesses, and proposed that taxpayers be permitted to file the T-106 and T-1134 forms electronically. The Chartered Professional Accountants of Canada requested that business financial data be standardized for electronic filing, which would reduce the compliance burden for businesses. In speaking about disputes between taxpayers and the Canada Revenue Agency, Tax Executives Institute, Inc. noted that such disputes cause delays and uncertainty, and requested that the Agency be permitted to settle disputes based on an assessment of the likelihood that the Minister of National Revenue would be unsuccessful in legal proceedings. c. International TaxationIn suggesting that significant federal tax revenue is located in offshore jurisdictions, Mr. Cockfield requested that the government invest in identifying offshore tax evaders. Similarly, Canadians for Tax Fairness encouraged greater federal efforts to reduce the use of tax havens by Canadians, including through increased disclosure of offshore investments. Brigitte Alepin – who is with Agora Fiscalité and appeared as an individual – noted the lowering of corporate tax rates in a number of jurisdictions; she called for the convening of a conference that would enable discussions among Canada and other countries, perhaps leading to the harmonization of tax rates across countries. The Canadian Bankers Association supported a Canadian corporate tax rate that is internationally competitive. Tax Executive Institute, Inc. highlighted the recommendations made by the Organisation for Economic Co-operation and Development in relation to base erosion and profit shifting, and urged the government to implement recommendations only after assessing their potential impact on the Canadian economy. Deloitte proposed that changes occur only if Canada’s trading partners are implementing similar measures, and advocated targeted – rather than broadly worded – provisions. Finally, Canadians for Tax Fairness urged the government to implement these recommendations. d. Tax Treatment of Certain Businesses, Entities and IndividualsIn speaking about increased lending by credit unions, and their ability to raise capital for expansion when compared to corporations with publicly traded shares, Credit Union Central of Canada asked for the creation of a 5% capital growth tax credit; in its view, in the absence of this measure, credit unions would pay a higher effective tax rate than banks by 2017. The Investment Funds Institute of Canada indicated that group registered retirement savings plans and pooled registered pension plans are treated differently for tax and regulatory purposes; it requested that they be treated similarly with respect to payroll tax measures, auto-enrolment and the locking-in of employer contributions. To ensure that mutual funds are treated in the same manner as other businesses, the Investment Funds Institute of Canada suggested that such funds be treated more fairly for purposes of the Goods and Services Tax/Harmonized Sales Tax. It also proposed that interest income and income from foreign sources be eligible for the 13% corporate general rate reduction. The Portfolio Management Association of Canada believed that consumption taxes should not be imposed on retirement savings, and urged an exemption for investment management services or, in the alternative, efforts by the federal and provincial governments to remove or mitigate provincial disparities in relation to the provincial portion of the Harmonized Sales Tax. As a means of allowing individuals to save for longer periods of retirement, the Investment Funds Institute of Canada advocated a reduction in the mandatory minimum withdrawal amounts for registered retirement income funds and/or an increase in the age by which the initial mandatory withdrawal must occur. Similarly, the Conference for Advanced Life Underwriting asked for an increase in this age, and it provided various formulae for calculating the mandatory withdrawal amount. In highlighting the large amount of money that is being held by private foundations rather than used for charitable purposes, Ms. Alepin supported an increase in the annual disbursement rate by such foundations from 3.5% to 8%. Regarding the rules for investments in tax-sheltered savings plans, the Portfolio Management Association of Canada proposed that the Income Tax Act’s list of designated exchanges be expanded to include shares listed on stock exchanges in South Korea, Russia and Brazil. e. Tax Incentives for Individuals and FamiliesIn commenting on tax relief, Frances Woolley – who is with Carleton University and appeared as an individual – and the Canadian Centre for Policy Alternatives urged the government not to proceed with tax reductions. The Investment Funds Institute of Canada focused on tax incentives for retirement saving, and advocated an increase in the contribution limit for Tax-Free Savings Accounts to $10,000 annually once the federal budget is balanced. To increase investments by individuals in small businesses, the Investment Industry Association of Canada proposed the creation of a capital gains rollover for individuals who sell shares in and, within six months, purchase shares in a small Canadian business. Jennifer Robson – who is with Carleton University and appeared as an individual – noted that the current tax incentives for personal savings favour high-income individuals, and advocated more tax assistance for households with low or modest wealth. The Conference for Advanced Life Underwriting urged the government to educate Canadians about their financial obligations relating to long-term care services, and to ensure that tax rules encourage more Canadians to purchase individual long-term health care insurance. It mentioned, in particular, tax-exempt registered retirement savings plan withdrawals to purchase such insurance. Imagine Canada requested the creation of a “stretch tax credit” that would provide an enhanced charitable donation tax credit to individuals who donate an amount in a given taxation year that exceeds their donation in the immediately preceding taxation year. In the view of Mr. Moffat, the administrative burden associated with tax expenditures is high, and numerous personal tax expenditures could be repealed and replaced with lower income tax rates, a higher Universal Child Care Benefit and/or a more generous Goods and Services Tax/Harmonized Sales Tax credit. In speaking about the Goods and Services Tax/Harmonized Sales Tax credit, Mr. Cockfield noted that low-income individuals who do not file a tax return do not receive the credit; he urged the creation of a program for Canada that is similar to the United States’ volunteer tax assistance program. Ms. Robson highlighted that tax relief can be provided in a range of ways, and urged consultation and widespread agreement among Canadians – and an analysis of the administrative and implementation burden – before a fundamental shift occurs in the calculation of the tax liability of individuals with families. Ms. Woolley noted that family income splitting raises the marginal tax rate imposed on the lower-earning spouse, and – as an alternative – advocated a new program for families with children that would combine the best features of the Canada Child Tax Benefit and the Universal Child Care Benefit. The Institute of Marriage and Family Canada supported family income splitting as a measure that would – in its opinion – establish horizontal equity among families. 2. Regulatory Regime of Certain Sectorsa. Credit Card Transaction FeesIn highlighting that high credit card transaction fees affect the amount of donations received by charities, Imagine Canada urged the involvement of the charitable sector in negotiations for a voluntary arrangement to regulate transaction fees. Restaurants Canada highlighted the existence of high credit card transactions fees and the application of those fees on the sales tax portion of restaurant bills. It advocated a regulatory cap on interchange fees, with rules to prevent the introduction of other merchant fees to replace the revenue that is lost and to prohibit credit card companies from earning a fee from the collection of sales tax, as well as Goods and Services Tax/Harmonized Sales Tax, by businesses. b. SecuritiesWith a focus on securities regulation in Canada, the Portfolio Management Association of Canada highlighted the co-operative capital markets regulatory system; it urged the government to continue working towards participation in this system by all provincial securities regulators. Similarly, the Canadian Bankers Association supported the government’s efforts to harmonize securities regulation in Canada. c. CharitiesIn the view of Gareth Kirkby – who appeared as an individual – the Canada Revenue Agency is auditing charities that have public policy preferences that differ from those of the government. He called for abolition of the Agency’s political activities audit program, encouraged greater clarity in the Income Tax Regulations definitions that pertain to charities, and proposed that the Canada Revenue Agency provide charities with the criteria it uses to evaluate charitable activities. d. Financial Services Provided by the Federal GovernmentImagine Canada suggested that charitable organizations face regulatory and administrative restrictions that limit their access to federal business development services provided to private-sector businesses; it called for these restrictions to be removed. C. Changes Proposed by Witnesses Invited to Address Topics Other Than “Improving Canada’s Taxation and Regulatory Regimes”The Committee’s witnesses were invited to speak about a particular topic. When they appeared, they often made comments about one of the other five topics selected by the Committee, as indicated below. 1. “Balancing the Federal Budget to Ensure Fiscal Sustainability and Economic Growth” WitnessesThe Canadian Council of Chief Executives, the Conference Board of Canada and the Canadian Taxpayers Federation called for a comprehensive review of the tax system with a view to simplifying it and supporting economic growth. As a way to increase financing for new businesses, the Fraser Institute proposed the elimination of – or, under certain conditions, the deferral of – taxes on capitals gains. The Canadian Taxpayers Federation supported a mechanism that would allow the averaging of capital gains income over a number of years so as to avoid taxation of the full amount of the gains when assets are sold. The Canadian Taxpayers Federation advocated a reduction in both personal income tax rates and the number of tax brackets. Both it and the Frontier Centre for Public Policy advised against the introduction of new “boutique tax credits.” The Fraser Institute proposed the creation of a medium-term plan to increase the competitiveness – relative to other countries – of personal income taxation. The Canadian Union of Public Employees’ brief outlined a series of measures that would increase federal revenue. In particular, the brief proposed that the federal corporate tax rate be restored to 22% and that a number of tax measures be eliminated, including the stock option deduction, the capital gains deduction, the deduction for business meals and entertainment expenses, and those that favour the oil and gas and mining sectors. The brief also suggested that tax laws be enforced to a greater extent in order to combat tax evasion and the use of tax havens, a new personal income tax rate of 35% be introduced for income exceeding $250,000, the banking and financial sectors be taxed at a higher rate, and an inheritance tax on estates valued at more than $5 million be introduced. According to the Canadian Taxpayers Federation, in the event that the government decides to provide tax reductions to families, a $10,000 child care deduction available to stay-at-home parents should be considered, with the working parent remunerating the stay-at-home parent, who would claim the deduction. 2. “Supporting Families and Helping Vulnerable Canadians by Focusing on Health, Education and Training” WitnessesAs a means of increasing the maximum amount of the National Child Benefit, YWCA Canada said that federal tax expenditures in relation to tax credits that support families – such as the Universal Child Care Benefit and the Child Fitness Tax Credit – should be reallocated to the National Child Benefit. 3. “Increasing the Competitiveness of Canadian Businesses Through Research, Development, Innovation and Commercialization” WitnessesCanada’s Research-Based Pharmaceutical Companies urged immediate implementation of the intellectual property provisions in the comprehensive economic and trade agreement concluded by Canada and the European Union, and indicated that any additional measures regarding dual litigation should be subject to a policy consultation process with stakeholders. It also called for changes to the amendment contained in Bill C-17, An Act to amend the Food and Drugs Act, that would reduce the threshold for disclosure of confidential business information by Health Canada. The Canadian Vehicle Manufacturers’ Association mentioned the need to make the accelerated capital cost allowance competitive with comparable incentives in other jurisdictions. Similarly, in highlighting the difference in capital cost allowance rates between Canada and the United States, Canadian Manufacturers & Exporters suggested that the current 50% depreciation rate for manufacturing and processing machinery and equipment be made permanent. The Confédération des syndicats nationaux requested that the government reverse its decision regarding gradual elimination of the Labour-Sponsored Venture Capital Corporations Tax Credit. In identifying the need to provide financial support to businesses in all sectors, the Société de promotion économique de Rimouski requested that funding application processes be improved in order to make it easier for businesses and institutions to identify funding sources and to renew funding. In its brief, Canada’s Research-Based Pharmaceutical Companies proposed that Health Canada adopt a modern and comprehensive legislative and regulatory regime for the assessment, approval and monitoring of drug products in Canada, and that federal regulations be aligned with international best practices. 4. “Ensuring Prosperous and Secure Communities, Including Through Support for Infrastructure” WitnessesAs a means by which to encourage capital accumulation, the Canadian Life and Health Insurance Association proposed elimination of the capital tax on financial institutions. The Canadian Electricity Association supported greater regulatory alignment with the United States to improve the integration of the North American electricity system. 5. “Maximizing the Number and Types of Jobs for Canadians” WitnessesThe Canadian Federation of Independent Business suggested that the government lower the small business tax rate to 9% by 2015, and – in supporting the one-for-one rule – publicly release a comprehensive baseline count of its regulatory requirements. The Quebec Employers’ Council’s brief said that the one-for-one rule should apply to any new federal regulations for transportation, telecommunications and/or financial services. In its brief, the Canadian Chamber of Commerce advocated a comprehensive review of taxation and regulatory regimes in Canada with a view to creating more streamlined and efficient systems. As well, the brief urged the elimination of tax credits that are either not cost effective or not achieving their intended purpose, with the revenue gains used to reduce personal and corporate tax rates. The Canadian Chamber of Commerce’s brief also called for the federal government to facilitate a comprehensive internal trade agreement that would allow the sale of goods and services across provincial/territorial borders, regardless of differences in regulations or standards. To reduce administrative costs, the brief urged the federal government to work with the provinces/territories on a common regulatory framework for trade across these borders that would be clear, and that would have an accessible and affordable dispute-resolution mechanism. The Green Budget Coalition asked the government to renew the Clean Air Agenda beyond 2016, and to increase its adaptation funding to at least $45 million annually. The Retail Council of Canada and the Quebec Employers’ Council’s brief suggested that the government maintain a tariff regime that is internationally competitive, and – before new international trade agreements are implemented – provide training and disseminate information to businesses on the possible benefits of these agreements. In particular, the Retail Council of Canada proposed the elimination of tariffs applied on a range of essential food and clothing items imported into Canada; this change should be effective in January 2015, the date on which entitlement to the General Preferential Tariff will be withdrawn from all goods that originate in 72 higher-income and trade-competitive countries, such as China and India. It also urged the government to act on its commitment to reduce credit card transaction fees for merchants. The Quebec Employers’ Council urged the government to review its policies relating to international commerce that occurs through online sales, and to assess the impact of online international commercial activity on both the competitiveness of Canadian companies and federal tax revenue. With increases in Internet-based broadcasting, which is not subject to Canadian content regulations, the Canadian Arts Coalition called on Parliament to investigate revenue models that would support a comprehensive Canadian cultural digital strategy. To harmonize the tax treatment across the manufacturing sector and with competitor countries, the Canadian Gas Association and the Canadian Association of Petroleum Producers’ brief advocated an accelerated capital cost allowance rate for liquefied natural gas facilities. The Canadian Gas Association’s brief proposed a subsidy or tax incentive for natural gas as an alternative transportation fuel, such as through maintaining its current fuel excise tax exemption on liquefied natural gas and compressed natural gas. |